Recently I’ve become privy to a high yielding investment from Global X and its Nasdaq 100 covered call ETF (QYLD). Being primarily an options trader myself my interest was immediately peeked but I do have a question, is QYLD a good investment? To which my answer is it depends.

What I mean is its likely determined by how happy you are with the amount of capital you’ve already acquired. Are you nearing retirement and sitting on a multi-million dollar portfolio or are you just getting started with a few thousand. For the former, QYLD could make sense. The prospect of long term growth may not be of any real value but a consistent and sustainable income stream may be. For the later, QYLD is, in my opinion, of little to no value and is probably best to be avoided.

That said, lets run some numbers to be sure I’m not putting my foot squarely in my mouth. In this post we’ll conduct a couple of different experiments to determine when or if QYLD should ever be apart of our portfolio.

1. QYLD for Income Generation

Edward is a soon to be retiree and has an investment portfolio worth $2.5 million. Edward isn’t overly concerned with capital appreciation but does want to live off the dividends his investments produce. Is QYLD a good investment?

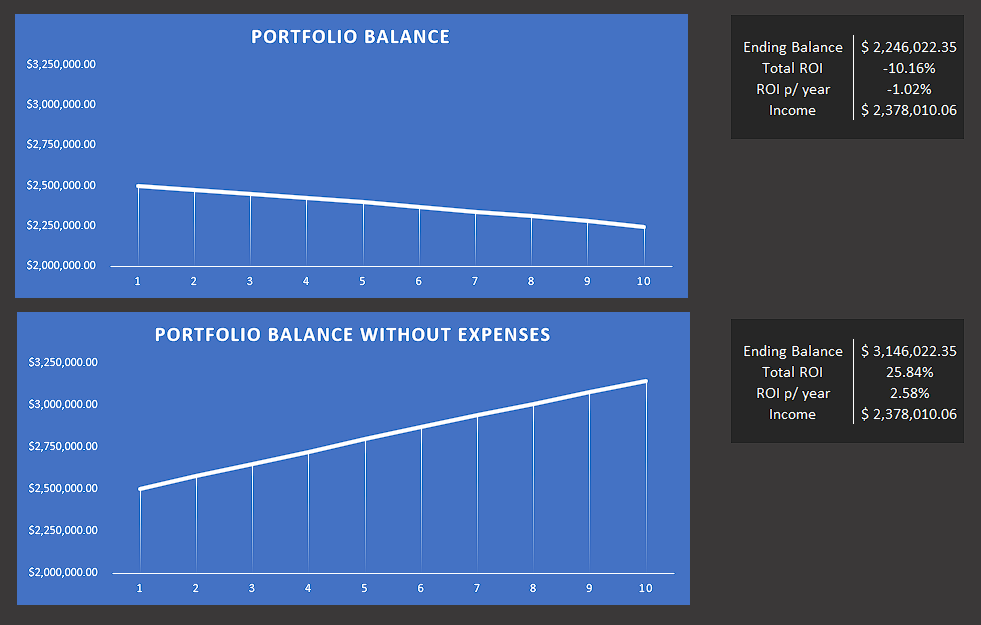

To answer that question, have a look at what might happen over the next 10 years if Edward were to invest his entire account into QYLD today. QYLD has an average yield of 14.08% according to SeekingAlpha.com.

To maintain a realistic expectation I’ve used an average yield of 10% per year, an average 5% capital depreciation per year, living expenses of $100,000 per year, and an annual inflation rate of 2%.

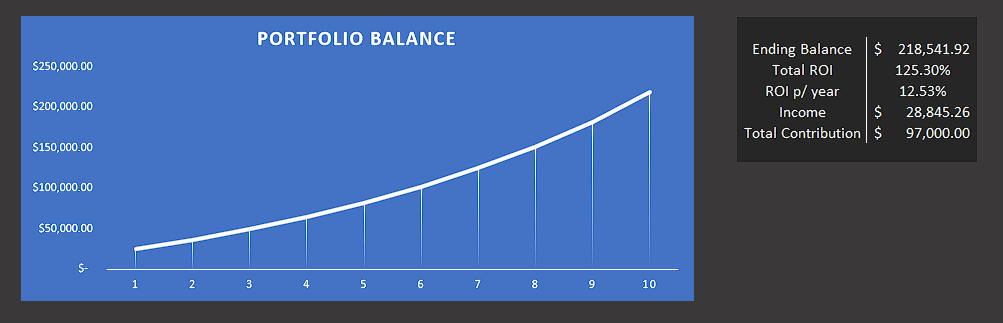

QYLD Investment in Retirement

You can see in the “Portfolio Balance” image above that as expected Edward’s account declined in value over the 10 year period. Adjusted for inflation Edward realized an overall loss of 10%. If Edward we’re able to reinvest his income, his account would have realized just over 25% in growth over the period. (Portfolio Balance without expenses)

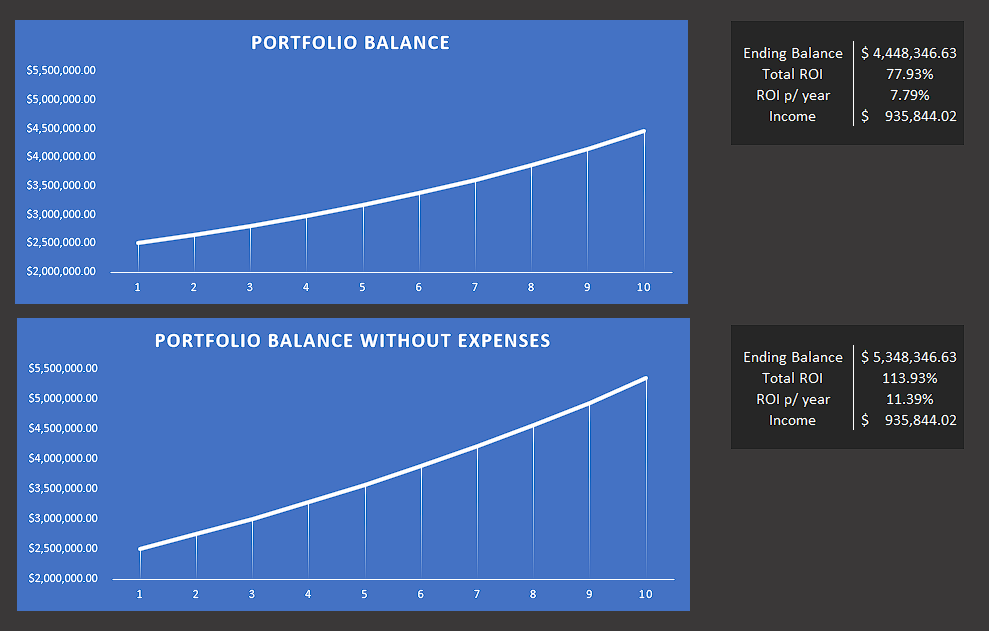

For comparison, here’s what Edwards portfolio would have looked like using the same metrics as before only using Coca-Cola (a well known Dividend Stalwart) instead of QYLD and Coca-Cola’s average return of 9%.

The key difference to consider is that Coca-Cola is NOT guaranteed to return 9% per year.

Coca-Cola Investment in Retirement

As you can see the income generated from this investment is less than half that of QYLD. Making QYLD favorable from that angle. From an overall perspective Coca-Cola would be much better returning 77% and 113% respectively. However, had Coca-Cola fallen on hard times and averaged a return of let’s say, 2% each year. Here’s how that might look.

Coca-Cola Investment During a Bear Market

As you can see, should Coca-Cola’s yearly figures begin to slip, QYLD offers a much more reliable income stream. Which I think answers the question, is QYLD a good investment? From this perspective, Yes, but the trade off is that going into the investment you know you’ve forfeited any bull market advance. Should the market decline by a meaningful amount for a period of time then QYLD is the absolute favorite. Conversely, should the market advance by a meaningful amount you’ll have missed out on literally all of the upside.

2. QYLD for Growth

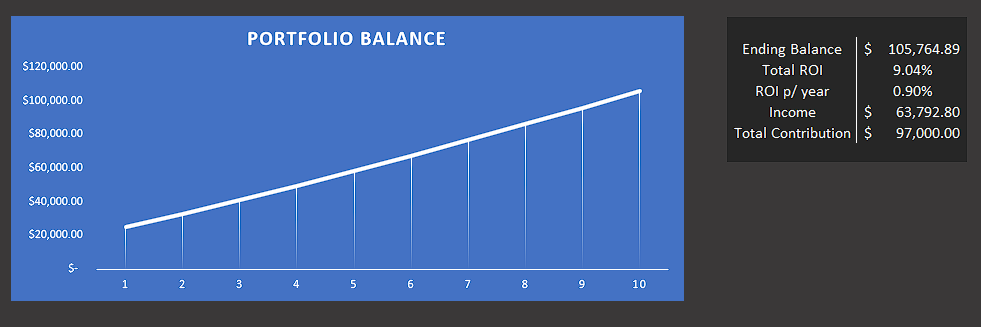

Susanna is a 28 year old teacher who longs to retire and live the life of her dreams but knows that if that’s ever going to happen she’ll have to save and compound her growth. Susanna wants to watch her portfolio grow by the maximum amount possible over the next 10 years. She has $25,000 available to invest today. Is QYLD a good Investment?

Using the same criteria as above, I’ll consider a 5% reduction in QYLD, a 10% yield, and 2% inflation annually. Notice, Susanna will not need the income for living expenses as that would come from her job as a teacher. She will however contribute $600 per month or $7200 each year for the 10 year period.

QYLD Investment for Growth Portfolio

The above chart only highlights the achilles heel of QYLD which we’ve already uncovered, it doesn’t grow. Taking into account the amount Susanna is investing each year the return of less than 1% is actually worse than could be received from a high yield checking account that faces no investment risk. For Susanna, QYLD is a definitive NO!

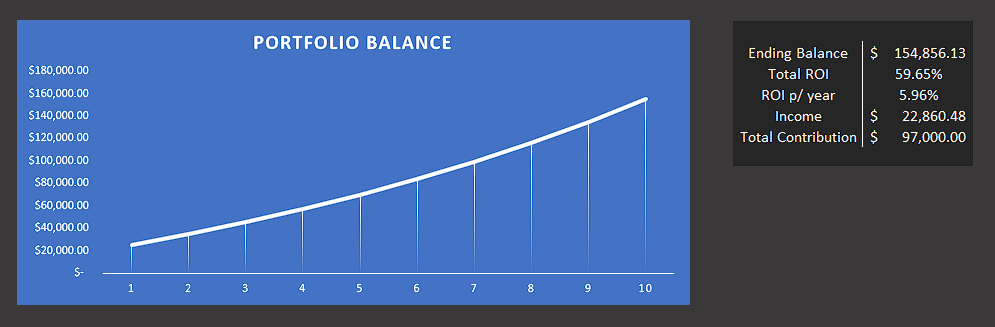

Had Susanna invested in Coca-Cola for the same period using their historical return figures her portfolio could look like this.

Coca-Cola Investment for Growth Portfolio

Accounting for inflation and a substantially lower dividend income stream Susanna would have still been rewarded with approximately $50,000 more dollars than if she had invested in QYLD.

To avoid redundancy I won’t post what the returns would be if Coca-Cola underperformed the market. I’ve done the test and they are similar to having invested in QYLD. However, let’s assume Susanna is an excellent stock picker and is able to beat the 9% average returned by the S&P 500 each year. If Susanna is able to return 15% each year by buying when Coca-Cola dips and selling when it advances, here’s how that could look.

Coca-Cola Investment for Growth Portfolio During Bull Market

Should Susanna find out she’s able to return 15% per year continually she would have watched her investment more than double in size during the period.

Is QYLD a GOOD Investment? It Depends but Mostly, No

As I hope is evidenced in the charts above QYLD fails to meet any reasonable investment goal for most everyone. At least any goal I have. Outside of the retiree that only wishes to earn a stable income on the capital he/she already has QYLD would NOT be a good investment opportunity. Moreover, QYLD failed to achieve the same return as a no risk savings account for the growth minded investor. In that light alone I think its obvious QYLD isn’t worth our time, or our dime.

What do you think? Have a missed the mark with this post. Is QYLD actually a good investment? Let me know in the comments below.

God bless,

Jeff