Hello again, it feels like an eternity since I last wrote but I wanted to jump in today with an important concept. Portfolio insurance. Before I do, even more important is eternal insurance. None of the money we make through investing or earn in our lifetimes will travel with us when we leave this place. So, prepare today by asking Jesus to take control of your life and be your Lord and Savior. I can say with confidence, He is the ultimate insurance policy and you won’t be disappointed.

With that, I want to discuss the concept having having some level of portfolio protection in place. At all times. Portfolio protection is often cited as a drag on portfolio performance. And while that may be true, when the next crash comes, I’m guessing it won’t be much of a drag. In the short term it feels like hundreds or thousands of dollars wasted and in truth, it is. Still, the day is coming, we all know it, when things will begin tumbling.

When it happens, some level of protection will be required or years of saving and investing will be undone. Now, how you ultimately choose to protect your investments is up to you but long puts work for me. Some will hold gold, consumer staples, utilities, or even bitcoin but I don’t prefer that level of risk. I feel like we’ve all seen those “safe haven” stocks fall right along with the market too many times.

Thus, in today’s post I want to share with you my approach to portfolio insurance. For more information and for a much better written article have a look at this PDF from Patten & Patten. You’ll have to click the download PDF button to view but it’s well worth the read.

Post Agenda

Importance of Portfolio Insurance

Before I go on, I want to again reference the above link to the Patten & Patten website. They did a thorough job of not only highlighting the importance of portfolio protection but also providing data to support their conclusions. If the concept of protecting your investment portfolio is new, then it’s worth a few minutes of your time.

Scenario A

Imagine tomorrow you wake up to news that the market is crashing. The headline may read, “Market Implodes: Prepare for the Worst”. After seeing that headline you quickly open your brokerage platform to see that your portfolio is down 15% and the market has halted trading. You’re panicking and want to sell your holdings NOW but have to wait until trading resumes. Additionally, the platform is experiencing technical difficulties as everyone around the world frantically attempts the same desperate maneuver.

The market begins trading again and your portfolio falls another 10% before trading is halted again. At this point, you may or may not have been able to offload your shares with buyers seemingly non-existent. Your orders to close have been initiated but all you can do is wait for the fervor to subside. When it finally does, your shares are sold at a steep discount and the loss is etched into stone. The lost capital is gone for good and not coming back nearly as quickly as it just disappeared.

Scenario B

Now, imagine this same scenario but you held put options as a hedge. The headline catches you by surprise but a sense of calm takes the place of frantic maneuvering as you almost cheer the decline on. Knowing, when the market begins again you’ll be able to lock in thousand’s of percentage points in gains from those puts. The market may be down 15-25% but you’re looking at a meager 5% loss or possibly an overall gain. A much different picture and certainly less fear as the market falls mercilessly.

Portfolio Insurance – It’s Required!

This leads me to the obvious question. Which scenario would you rather endure? Are you comfortable navigating the unknown of a “Black Monday” style crash? Or would you prefer to avoid the emotional extreme of watching years flash before your very eyes?

I know where I would rather be when that eventually happens. I would rather be cashing in puts than sitting by wondering if my life savings has just been squandered. Thus, the importance of some form of protection cannot be overstated. Rather, the importance of protection is a requirement in today’s market.

We all know the fall is coming, we’ve know it for a while. Only so much political gesturing or Federal Reserve intervention can prop up a dead horse before people notice something is starting to smell. Still, we don’t know when or how or what will topple the first domino. So, it’s imperative we get prepared today and by any means necessary. At least that’s my sentiment.

How Much Insurance do I Need?

That of course leads us to the next big question. How much or how many is appropriate? Too much and I’ve wasted money, too little and I’ve merely enjoyed a great trade without much overall protection. These are questions that every investor wrestles with at some point in their investment journey.

Unfortunately, I’ve heard this quote many times, “Far more money has been lost preparing for corrections than in the corrections themselves”. This is a dangerous quote in my opinion. Rather than wrestle with the concept of portfolio protection, this quote suggests we just don’t worry about it at all. I know at one point in my own journey I saw this and thought, “I guess I’ll just accept the full risk”. If you’re honest, the same thought probably crossed your mind as well.

The reality though is this is true right up until the day it isn’t. Sure, covid worked out ok as we flooded the market with new money but imagine the covid decline without the immediate recovery. When that happens, I bet we don’t see this quote cited in such a positive light anymore.

Using a Volatility Graph to Determine How Much Insurance is Needed

“How much” is an important question and one I’ll attempt to answer by introducing you to the ThinkorSwim(TOS) Vol step graph. As a brief introduction, the risk profile tab on TOS is every option traders best friend. Set out of the box to +1 @Expiration. This simply shows the trader the P/L diagram for any options position with all factors exactly as they are today. However, when the market begins falling, volatility will go through the roof. Meaning, the cost to buy an option will skyrocket. The Vol step graph allows us to see graphically what can happen to our options as volatility changes.

+1 @Expiration Graph

At the top of the screen the “Lines” dropdown is set to +1 @Expiration. In this instance, if nothing else changes a 10% decline in SPY will return about $2,800 in profit. Not a great deal of protection for the next 61 days with a cost of $744 dollars. However, watch what that becomes when we account for volatility.

Shockingly, that $2800 dollar profit became $13,000 in profit when volatility is applied. Moreover, I left the volatility at a mild 40% increase. For context, volatility or VIX increased more than 70% from October 10, 2025 – October 17, 2025. An increase that didn’t come with a catastrophic market decline. For more context, the image below shows the volatility increase from the covid crash.

Apply that level of volatility increase to our $744 dollars of puts from the first image and here’s what the P/L diagram would become.

Just insane, for $744 dollars if the market craters we could be sitting on a put profit of almost $100,000 dollars! More than capable of protecting a portfolio. I know I would feel much better cashing in a put for $100k than I would just licking my wounds from a major market decline.

So, How Much do I Need?

Well, I showed you that process so you could begin testing and determine the exact answer for your own portfolio. In general, I think protecting somewhere near 50% of the portfolio is appropriate. However, you’ll have to balance that figure against how much capital you’ll want to commit to protection. Knowing that more often than not that capital will be lost, or a drag on the portfolio’s performance. Since the market generally moves higher.

For me, I usually want to hold 2-3 puts at any given time. I’ve accepted that my portfolio will still fall when the market declines but that at least gives me some protection for now. As you’ll see in the next section, my ability to protect is limited by the amount of income I can generate. If I wanted to pay for the protection out of my own pocket I would probably prefer to own 5-10 puts at all times. I’m building toward that as we speak and, like everyone else, hoping the crash doesn’t happen in the near future.

My Portfolio Insurance Plan

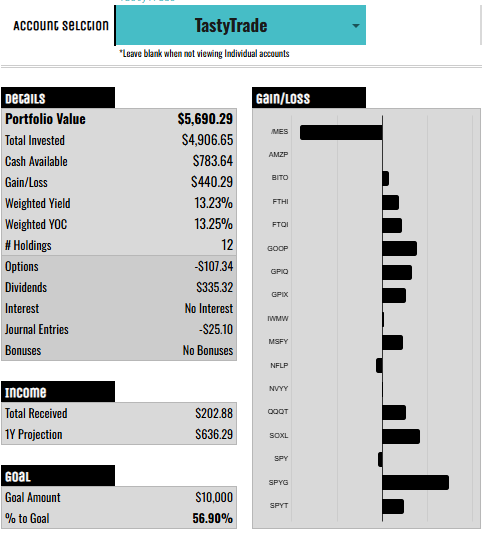

I won’t be long here. My plan is pretty simple. I’ve taken $5,000 dollars from my savings and put it into a TastyTrade account. Additionally, I contribute $150 each month to purchase income investments. Here is a screenshot of the portfolio’s statistics from my trading journal today.

A few things I want to highlight as we look at this portfolio. First, my goal for the account is $10.000. Moreover, I’ve included the holdings gain/loss graph to show the different investments and their performance. I realize there isn’t a dollar figure attached but this provides a general idea of how things are performing. I always want to keep my options costs to a figure below my total income received. Meaning, the options are financed via income.

Currently, my yield on cost(YOC) is 13.25% per year or 1.1% per month. When the account eventually reaches $10,000 that will yield about $100 per month in dividends. From there, most of that income will be used to continually buy puts. If excess income exists I’ll reinvest it to grow my income further.

Hopefully, growing the account as my overall portfolio grows and thus my level of protection. For now, I try to buy puts with about 100 DTE so that I have them on the books should the market turn down. In the future though, I’d like to purchase puts monthly to avoid some of the time premium I’m currently having to pay for.

One final note before I close, you’ll notice I’ve left some capital as cash. I use that capital to sell way OTM puts on SOXL and to keep some powder dry. The thought being, if the market does fall I can scoop up additional income producers at rock bottom prices.

Final Thoughts

To close, my hope is everyone that stumbles onto this post will take a moment to consider their own level of portfolio protection. To often, this becomes an afterthought as we test and assess various investments or strategies. I think, myself included, we’re all really good about doing our research on the frontend but maybe don’t spend enough time protecting the investment once we’ve committed the capital.

Sure, one camp would say just ride the wave and time in the market will make up for any temporary fall. Though, I can’t help but wonder how I might feel about my financial future when the market does eventually retrace 50% or more. I know I for one would greatly appreciate the psychological and financial win at a time when its sure to seem like all hope is lost.

Finally, before I sign off today, if you’re curious about my full investment methodology I wrote a post earlier this year titled, “An Investment Playbook for Today’s Markets”. Inside I provide a high level overview of my investment philosophy and I couple the strategy discussed here with that approach for portfolio insurance.

Until the next post.

God bless,

Jeff